Comprehensive Energy Data Intelligence

Information About Energy Companies, Their Assets, Market Deals, Industry Documents and More...

SCOOP/STACK Midstream Developments. Pipeline Projects Driving Gas Prices. Challenge of Getting Water for Fracking

12/20/2018

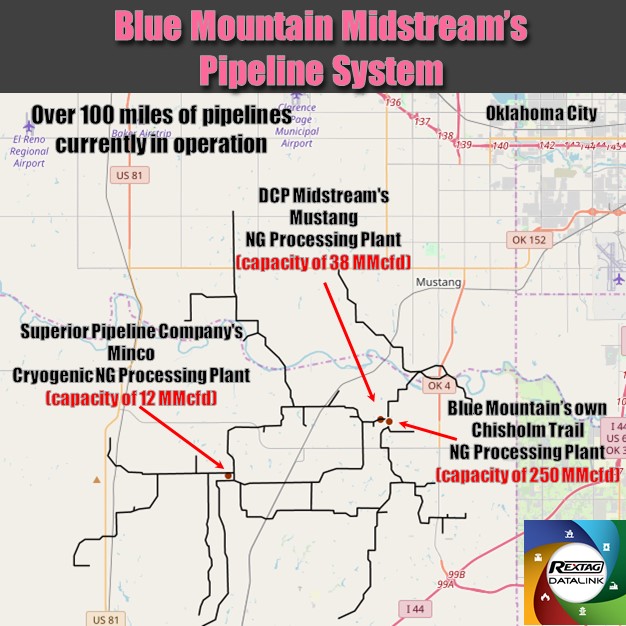

Positive Outlook on SCOOP / STACK’s Blue Mountain Midstream’s Pipeline System

Blue Mountain Midstream LLC Company operating in Merge play as well as in SCOOP and STACK plays, OK, continues to be a “fast-growing business”. Being a 100% subsidiary of the Riviera Resources, Inc., a recent spin-off from Linn Energy, Blue Mountain Midstream is said by David Rottino, Riviera’s president and CEO, during the recent company’s earnings call to remain one of its “tremendous growth assets”.

Blue Mountain provides natural gas, crude oil and natural gas liquids service solutions in the mentioned area. (See this on Rextag's map above).

Christmas Season Decorative Lighting and Power Demand. Does This Still Affect Gas Prices? (Or Have New Pipeline Projects Changed this Pattern?)

According to research (by EnVantage Inc.), a 10% increase in power demand near Christmas and the New Year was historically attributed to decorative lighting. Although diminishing due to the slow adoption of LED, this year the effect is hard to trace due to extreme volatility. Waha Hub prices were fluctuating from $3.85 /MMBtu on Nov. 13 down to $0.30 /MMBtu in two weeks and up to $1.36 /MMBtu by December 4.

Most of the movement is attributed to the excessive gas supply from Midland basin. The latter was a by-product (associated gas) from additional oil output delivered from Midland to Colorado City and Wichita Falls along newly introduced Sunrise Pipeline expansion by Plains All American LP. Estimated at over 750 MMcfd it contributed to the Waha plunging prices.

NGL prices likewise are thought to be affected by prospects of another group of pipelines under construction: Mariner East 1 and Mariner East 2 pipelines by Sunoco. Located in Pennsylvania, the pipelines are intended to facilitate the transfer of Natural Gas Liquids from the Utica and Marcellus Shale Formations to ports on the East, where ethane, butane, pentane, propane mixes will be exported.

Fracking Water Demand: Challenges and Their Treatment Approaches

It has been pointed out by experts that “rig count correlates with water source needs”. If a region lacks water-handling assets then development slows to a stop. Companies need to procure both water to drill and means of its future disposal. Cost is the main concern here.

The issue may be resolved by one of the following approaches:

- Adjusting the existing pipelines to become water-dedicated for bringing new water to the area.

- Use treated water from nearby municipals. (Several projects are being discussed in Oklahoma City in the Midcontinent, Carlsbad, N.M., and Odessa and Midland, Texas). However, supply of the treated water is quite limited so this will remain a niche market.

- Reuse of already produced water for frack jobs. This approach can be taken by regional players who would provide dedicated systems in place to handle all: gas, oil and water for their local customers.

If you are looking for more information about energy companies, their assets, and energy deals, please, contact our sales office mapping@hartenergy.com, Tel. 619-349-4970 or SCHEDULE A DEMO to learn how Rextag can help you leverage energy data for your business.

LIVE: Permian Highlights Discussed Online by Rextag (Hart Energy) Data Experts

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/Permian_infrastructure_2019.png)

How has the Permian basin been performing recently? Does production keep growing? Who are the top market players? Find out with Rextag data experts.

Let’s Take a Step Into The Future: Water Management

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/Water-management.jpg)

As demands for water management solutions increase, service companies are looking for new ways to optimize their ability to recycle and store this water.

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/278_Blog_US Leads Global Oil and Gas Production, US Drillers Cut Rigs Again and 1.4 Million BBL Decrease (1).jpg)

The U.S. has overtaken Saudi Arabia and Russia to become the world's largest oil and gas producer. In 2024, America's oil output has surpassed last year's record by 1.4%, reaching new heights. Even as oil-producing countries in the Middle East cut back, the U.S. continued to ramp up production after a downturn in 2020, establishing itself as a dominant force in the global market. In terms of numbers, U.S. oil production jumped from an average of 2.93 million barrels per day in 2023 to 13.12 million barrels per day in 2024, marking a significant 7.1% increase.

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/276_Blog_Midstream Giant Kinetik Launches $1.3B M&A to Acquire Durango in the Delaware Basin.jpg)

Kinetik Holdings recently announced a series of transactions in the energy sector. They struck a deal to buy Durango Permian infrastructure for $765 million. At the same time, they're selling their 16% share in the Gulf Coast Express Pipeline to ArcLight Capital Partners for $540 million. The total purchase cost includes $510 million in cash paid immediately and an additional $30 million that will be paid later, depending on whether they decide to expand further.

![$data['article']['post_image_alt']](https://images2.rextag.com/public/blog/275_Blog_Permian Basin- Oxy Shops Delaware Assets (1).jpg)

Recently, the Permian has seen significant acquisitions: Exxon Mobil purchased Pioneer Natural Resources for about $60 billion. Diamondback Energy's $26 billion deal to acquire Endeavor Energy Resources is currently on hold due to requests from the U.S. Federal Trade Commission. Occidental’s acquisition of CrownRock for $12 billion in the Midland.